Navigating Rates

Commodities: unearthing opportunities

Elevated geopolitical tensions, the transition to a cleaner global economy and the policies of US President Donald Trump may shape commodity markets in 2025. With further swings in the market possible, a nimble approach to managing allocation may serve investors well and further strengthen the diversification benefits commodities can bring to a portfolio.

Key takeaways

- Among base metals, we’re most optimistic about the outlook for copper. As a component of batteries, motors and cables critical to the energy transition, we expect continued demand for copper in 2025 and beyond, with scarce supply likely to support prices.

- Gold outshone other asset classes over the past two years, and we expect further gains amid a structural shift in the market. In energy markets, our favourite pick is US natural gas, and we anticipate steps taken by the Trump administration to support gas prices further.

- With higher inflation a key risk in 2025, commodities can provide a hedge to inflation surprises as their prices tend to climb when the prices of the goods and services they produce rise. Another key feature of commodities is their diversification benefit due to their low correlation to equity and bond returns.

The ground beneath the commodities market is shifting. Geopolitical tensions and decarbonisation are changing the outlook for everything from oil to copper, while inflation and the possible rollout of US tariffs are other factors that may tip the commodity market’s supply-demand balance in 2025.

We see an uneven outlook for commodities in the year ahead – but with further swings in the market possible, a nimble approach to managing allocation may serve investors well. Here are four of the main commodities on our radar in 2025:

Copper: supply issues support the base metal of electrification

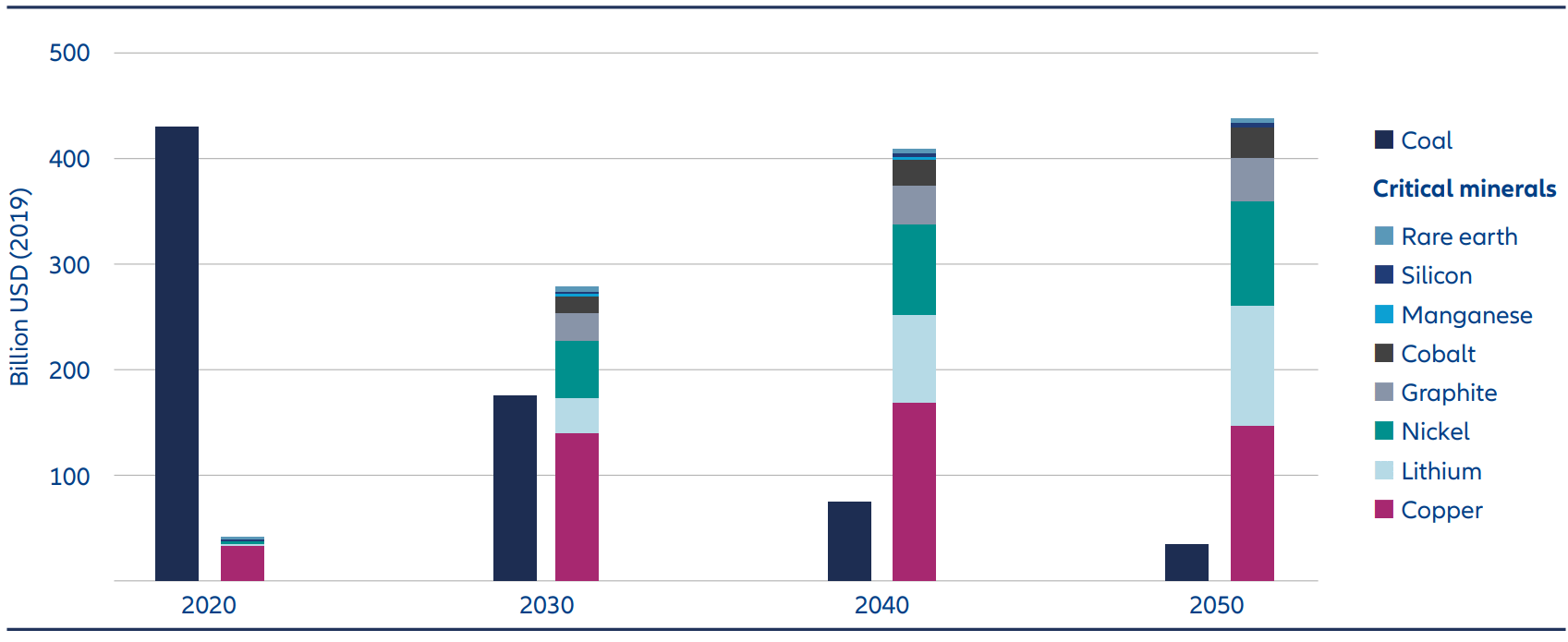

Among base metals, we’re most optimistic about the outlook for copper. Copper, along with other critical minerals, has a major role in the global economy’s move from fossil fuels to greener energy sources as a component of batteries, motors and cables integral to the energy transition (see Exhibit 1). We see the lion’s share of this demand in China, the largest metals market.

Current copper supply remains scarce as mine supply growth is limited. Many analysts expect to see mining fully resume in 2025 at the large Cobre Panama mine, which contributed around 1.5% of global copper supply in previous years, after its closure two years ago. But we’re sceptical that it will re-open at full capacity, given the strength of public feeling about its environmental impact. Even if operations at the mine resume in 2025, the supply of copper is likely to be insufficient. The primary supply of copper is set to fall short of demand up to 2027, forecasts BloombergNEF, with 2025’s deficit likely to be similar to the 4.6 million tonnes in 2021.

Trump administration policies may not dim copper’s role in the green transition

One factor to watch in 2025 will be the impact of policies of US President Donald Trump. Mr Trump has said he intends to impose high tariffs on goods imported into the US, potentially slowing down the global economy. But the silver lining of any tariffs might be the response of China’s government, including the possible roll out of further stimulus and investments in green sectors –most likely renewable energies, electric vehicles (EVs) and power grid infrastructure.

Mr Trump’s policy agenda raises uncertainty about the future funding of new US infrastructure projects related to the green transition. His administration will likely reduce subsidies for renewable energies and cut the carbon targets in the transport sector, therefore eliminating the advantage of EVs over internal combustion engine cars in the US. But despite these measures, we think utility companies will expand the power grid (even in the US) due to higher power demand from data centres, solid economic growth, and crypto mining. Power grid expansion and further electrification are also a key driver for copper demand in Europe.

Exhibit 1: Copper and other critical minerals are set to help fuel the energy transition

Source: International Energy Agency – Net Zero by 2050, May 2021. The statements contained herein may include statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. We assume no obligation to update any forward-looking statement. Note: Includes total revenue for coal and for selected critical minerals used in clean energy technologies. The prices of critical minerals are based on conservative assumptions about cost increases (around a 10%-20% increase from current levels to 2050).

Gold: geopolitics, fiscal worries to sustain the gold rush

Gold was the standout performer across all asset classes in 2024 – and we anticipate further gains in 2025. Traditionally seen as a safe-haven asset, gold’s strong performance has been unexpected in a context where economic growth usually supports equities and energy markets. Our analysis shows gold’s rise has been due to a structural shift in the market, supported by worries about rising fiscal deficits and increased central bank buying, underpinned by heightened geopolitical concerns. In our view, these factors have supplanted the traditional drivers of gold’s price: US dollar weakness, low real yields and increased demand from retail investors.

We anticipate that gold prices will continue to decouple from interest rates and real yields, especially if structural factors like de-dollarisation and fiscal spending concerns persist.

In the near term, lack of clarity about significant parts of Mr Trump’s policy agenda – including potential tariffs – may generate financial market volatility, providing upward momentum to perceived safe havens such as gold.

Oil: challenges to “drill, baby, drill”

We’re cautious about the outlook for oil, given the likelihood of higher supply. Oil prices were supported by the Organisation of the Petroleum Exporting Countries (OPEC+) production cuts in 2024, but the cartel has announced plans to reverse the cuts in 2025. Supply from non-OPEC+ members is also set to rise. ExxonMobil’s project in Guyana will contribute additional capacity. Brazil may increase production further, and the US, under the Trump administration and its “drill, baby, drill” mantra, will also ramp up production.

Markets will be carefully watching the Trump administration’s production growth target of 3 million barrels per day (up from the current annual average growth pace of 1.8 million barrels per day between 2018 and 2023, according to Goldman Sachs). In our view, the target seems challenging in the short term due to two main factors:

- US oil producers lack incentives to increase capital expenditure and production, preferring to maintain record-high cash reserves and dividend payments.

- Ramping up oil production requires long-term infrastructure investment. At least for now, we see no signs of that investment materialising.

Although oil demand may still rise in 2025, China’s growing appetite for oil should slow in the coming years as the economy seeks to become less reliant on hydrocarbons.

In summary, oil prices in 2025 are likely to be primarily influenced by supply dynamics. Geopolitical developments may inject volatility. An example might be further US sanctions on the Russian shadow fleet of ships transporting oil.

Natural gas: demand hotting up

In energy markets, our favourite pick is US natural gas. Although inventories remain at relatively high levels, recent prices have been propelled by cold weather in the US, raising heating demand.

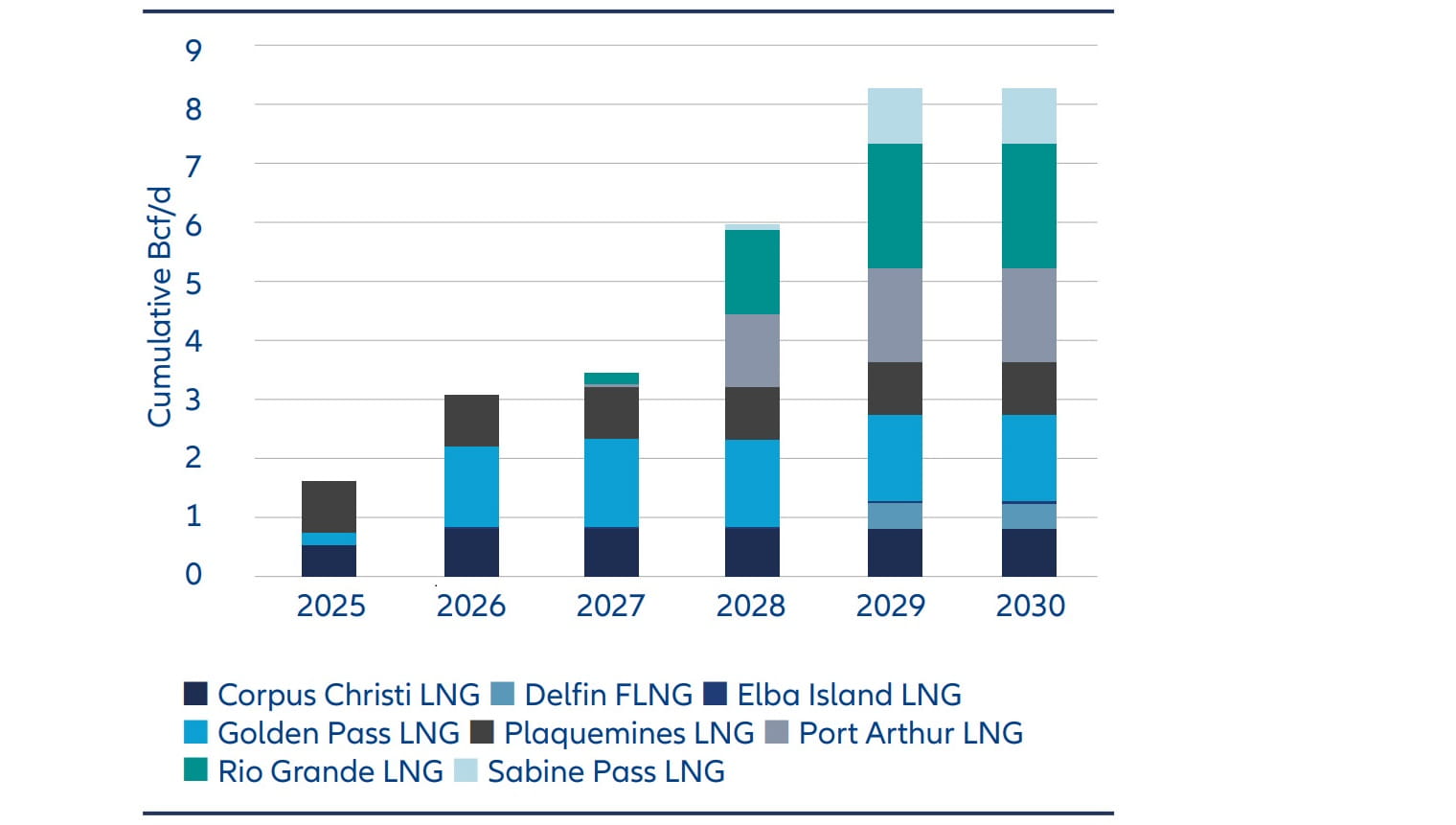

We anticipate steps taken by the Trump administration to support gas prices further. The US is expected to lift liquid natural gas (LNG) export restrictions, leading to a rise in LNG export capacities over the next few years (see Exhibit 2). We expect this extra capacity, alongside the expansion of gas-powered plants in the US, to meet rising electricity demand, particularly from artificial intelligence data centres and crypto mining.

The unknown factor for oil and gas prices is the potential for US tariffs on Canadian and Mexico’s oil and gas imports. Given our belief that the US production target cannot be fully achieved straightaway, one immediate impact from tariffs could be higher energy prices, with US consumers likely bearing the inflationary costs, at least in the short term, if energy output remains unchanged elsewhere.

Exhibit 2: US LNG producers’ capacity to export is set to surge

Source: S&P; Citi Commodities, September 2024

Commodities: diversification benefits

The potential for unexpected increases in inflation is an important reason to consider commodities as part of a diversified portfolio. Commodities can provide a hedge to surprises in inflation as their prices tend to climb when the prices of the goods and services they produce rise in response to higher demand. Inflation can sometimes be triggered by rising commodity prices – for example, oil prices tend to climb when oil inventories are low in an environment of rising demand. The increase in oil prices can push up the price of goods and services, fanning inflation.

A one percentage point unexpected rise in US inflation has, on average, led to a real (inflation-adjusted) return gain of seven percentage points for commodities, Goldman Sachs research shows. Higher inflation is a key risk in 2025, in our view, because of lower taxes in the US and possible stimulus in China. Commodities perform less well in a recession, but that environment is not our base case scenario.

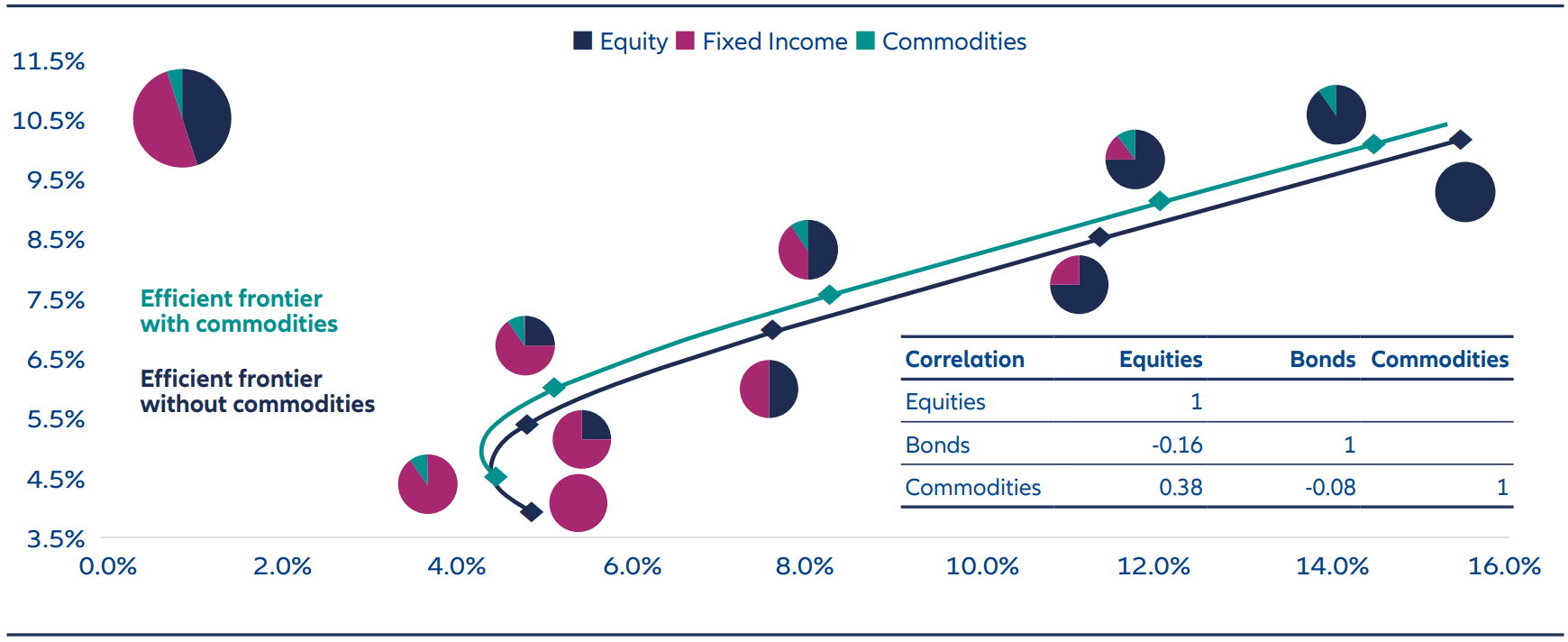

Another key feature of commodities is their diversification benefit due to their low correlation to equity and bond returns. Our analysis shows adding a 10% allocation to commodities in a portfolio made up of fixed income and equities may provide higher expected returns than a portfolio without it (see Exhibit 3).

In summary, although we’re watching the potential for market swings posed by tariffs and other geopolitical risks, we expect 2025 to be a year that underlines the value commodities can bring to a balanced portfolio.

Exhibit 3: Commodities can provide a useful diversifier to a multi asset portfolio

Source: Allianz Global Investors; For illustration purposes; data as per 30.09.2024. The information presented represents the historical returns of various allocations among US Equities (S&P500), US Government Bonds (10y) and Commodities (Bcom ex Ags/Live F6) for a time period between 12/1997 through 02/2022. Past performance does not predict future returns. The information and charts above are provided for illustrative purposes only. The charts do not reflect actual data or show actual performance and are not indicative of future performance. See additional disclosure at the end of this presentation. Investors cannot invest directly into an index. Diversification does not guarantee a profit or protect against losses.

4225597